Debit vs. Credit: Everything You Need to Know

What is the Core Difference Between Debits and Credits?

In double-entry bookkeeping, a debit (DR) is an entry that records financial value coming into an account (increasing assets or expenses on the left side of the ledger), while a credit (CR) records value going out (increasing revenue, liabilities, or equity on the right side). For your business books to remain accurate and legally compliant, every single financial transaction must have equal and opposing debit and credit entries.

To help you master your bookkeeping without the complex accounting jargon, this guide will walk you through the essential foundations of financial tracking:

- Creditors vs. Debtors: The exact commercial definitions of these entities and when a person or business is legally considered either.

- The Double-Entry System: How accounting mechanics map every financial transaction to the left and right sides of your general ledger.

- Financial Statement Impact: The specific ways debit and credit balances directly alter your Assets, Liabilities, and Equity on the Balance Sheet.

- Everyday Practical Examples: Step-by-step transaction breakdowns covering sales invoicing, receiving payments, and splitting a 15% VAT entry.

- Automated Bookkeeping: How utilizing modern cloud accounting software removes manual double-entry errors entirely.

What is the Difference Between a Creditor and a Debtor?

- Meaning of a Creditor: A creditor is an individual or entity that extends a loan or sells goods or services on credit, expecting to receive payments in the future. In other words, a creditor is the party that provides money or credit and expects it to be repaid at a later date, with or without interest. For example, if you give a loan to a friend, you become the creditor because they owe you the amount they borrowed.

- Meaning of a Debtor: A debtor is an individual or entity that receives a loan or purchases goods or services on credit, assuming the obligation to make future payments. In other words, a debtor is the party that receives money or credit and is bound to repay it in the future, with or without interest.

Debit vs. Credit: A Basic Overview

Debit and Credit are the basic units of the double-entry accounting method, which was developed by a Franciscan monk named Luca Pacioli. Pacioli is now called the "Father of Accounting" because the method he came up with is still used today.

The terms debit (DR) and credit (CR) have Latin origins. Debit originated from debitum, which means "what is due," and credit comes from creditum, meaning "something given to someone or a loan."

There are a few ideas about what the letters DR and CR stand for when they stand for debit and credit. One theory says that the DR and CR emerge from the Latin words debere and credere, which are the present active forms of the 'debitum and creditum' words. Another idea is that DR stands for "debit record," and CR stands for "credit record."

A "CR" is written on the account when liabilities or shareholders' equity go up. When liabilities go down, we talk about a debit, which is abbreviated as "DR."

Get 30% Off Wafeq yearly packages

Enter your email to receive your exclusive discount code. New users only!

Read more about: Accounting basics with a complete overview.

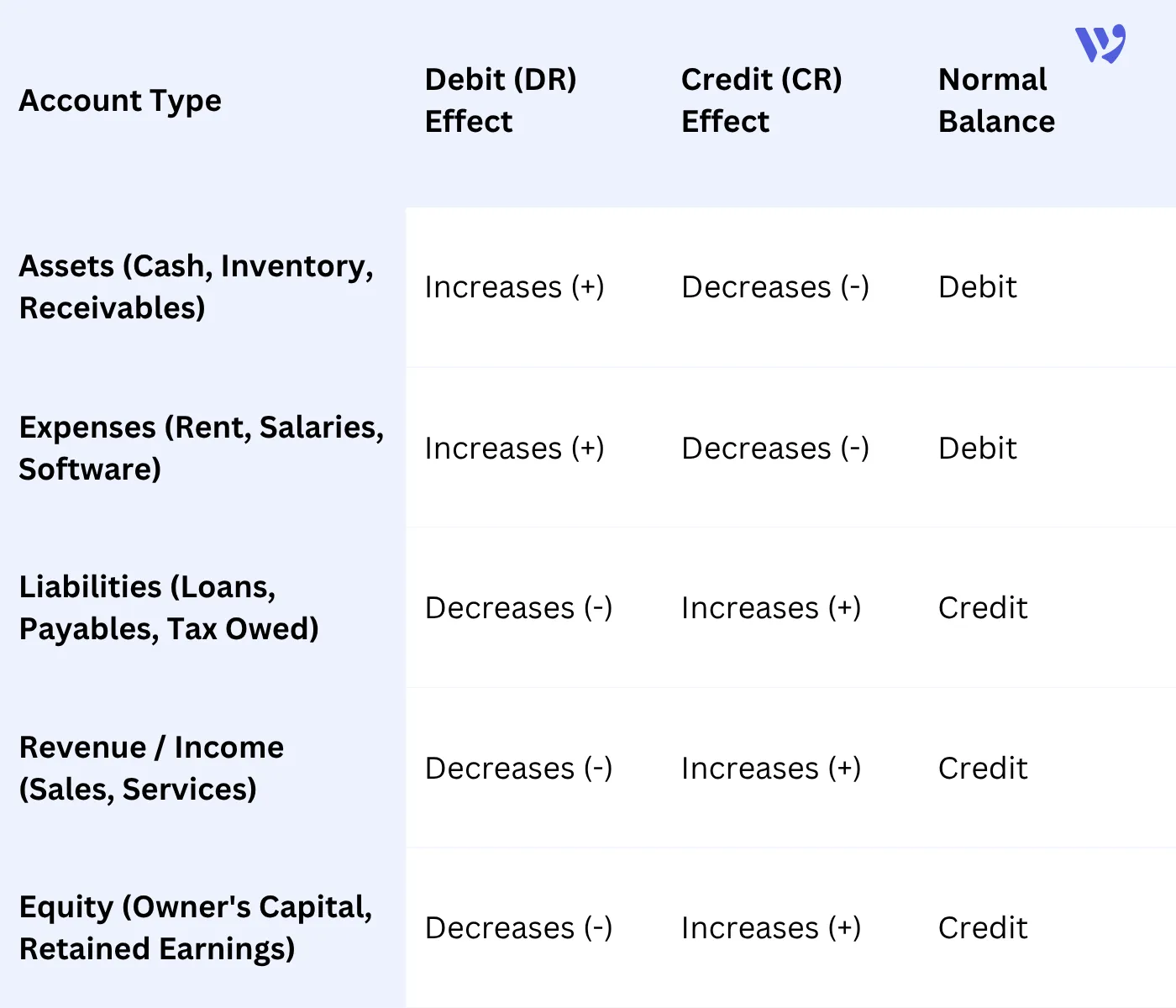

Quick Reference: How Debits and Credits Affect Accounts

To keep your books balanced, you need to know how a debit or credit changes the value of an account. Use this cheat sheet as a quick guide:

Fast Facts about Debits and Credits:

- Left vs. Right: Debits always sit on the left side of a ledger; Credits always sit on the right.

- The Golden Rule: Total debits must always equal total credits for every transaction to keep books balanced.

- Asset Behavior: Liquid cash and accounts receivable grow with debits and shrink with credits.

- Liability Behavior: Supplier bills and bank loans grow with credits and shrink with debits.

Practical Examples: Debits and Credits in Everyday Transactions

Let's go over the fundamentals of Pacioli's method, also called "double-entry accounting. The first thing to mention is that assets must equal liabilities plus shareholders' equity on a balance sheet or in a ledger.

Assests = Liabilities + Shareholders' Equity

Assests = Liabilities + Shareholders' Equity

It's best to take a look at an example to see how this method works.

Example:

Example:

Company XYZ sends Client A an invoice. The company's accountant puts the invoice amount as a credit in the revenue section of the balance sheet and as a debit in the accounts receivable section. Both debit (left) and credit (right) sides received an entry, which complies with the double-entry method.

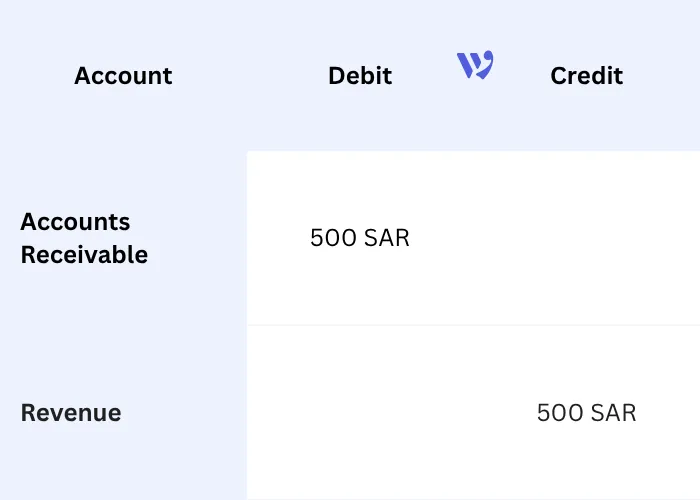

To see how double-entry accounting functions in daily business operations, let's track the two most common transactions every business handles: issuing a sales invoice and receiving its payment.

Transaction 1: Issuing a Sales Invoice

When you send an invoice for 500 SAR to a client for services rendered, your revenue increases, but you haven't received the physical cash yet.

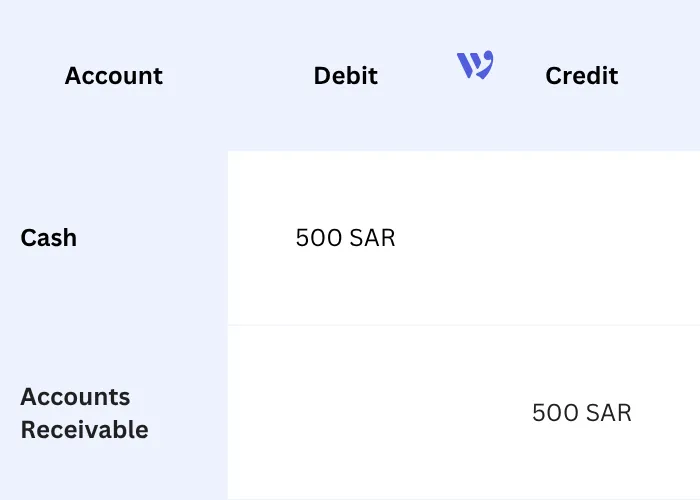

Transaction 2: Receiving the Invoice Payment

When the client pays that 500 SAR invoice into your business bank account, you must update your books to reflect that the debt is cleared and the cash has arrived.

When you debit assets, the change must be reflected on a credit account, too. On the other hand, an increase in liabilities (credit) needs to result in a corresponding debit in the appropriate account.

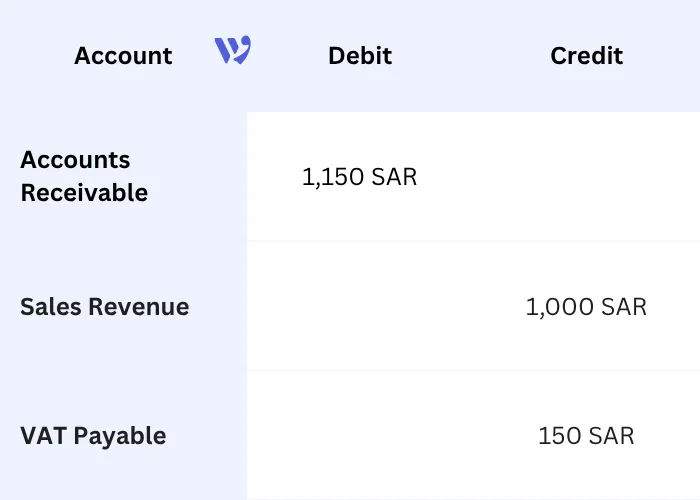

Transaction 3: Recording a Transaction with 15% VAT

When your business sells taxable goods or services in Saudi Arabia, you must account for the 15% Value Added Tax (VAT). This requires breaking the entry into three parts to track your actual sales separate from the tax you owe to ZATCA.

The Scenario: You issue a ZATCA-compliant e-invoice to a customer for services worth 1,000 SAR, plus 15% VAT (150 SAR), making the total invoice value 1,150 SAR.

The Journal Entry:

Tracking input and output VAT accounts manually increases your risk of delay penalties and costly audit errors.

Tracking input and output VAT accounts manually increases your risk of delay penalties and costly audit errors.

Wafeq Accounting removes this burden entirely. The moment you issue an e-invoice, the system automatically calculates the 15% VAT, maps it to the correct debit/credit accounts, and generates an audit-ready VAT return report for ZATCA in one click.

Use Of Double-Entry Accounting

The double-entry methodology is used by most businesses, even small ones with only one owner. This is because it lets you keep track of each business transaction in at least two accounts, giving a more accurate picture of your finances.

The way it works is simple:

A debit is put into at least one account, then a credit of the same amount is put into at least one account. Then, the two entries can be utilized to demonstrate how an external transaction affects the company’s finances. Ultimately, both the debit and credit sides need to equal one another to result in a book balance.

Read more about: Accounting Journals, Ledgers, and Double Entry.

As we can see, it is always at least two entries in double-entry accounting that balance a company's books and show net income, assets, liabilities, and more. There is one exception, though, as the income statement sometimes uses the single-entry method, normally not more than once a year.

With the double-entry method, every time a transaction is recorded, the books are updated, so the balance sheet is always correct. In short, the double-entry method is a great way of keeping track of where cash comes from and where it goes.

A reminder:

A reminder:

with the balance sheet, you can see your assets, liabilities, and owner's equity (net worth) at any given moment, but you only get a timely, static picture of your business's finances.

How To Record Debit And Credit

In your business's general ledger, both debits and credits are documented. A general ledger has a full record of all financial transactions that happened over a certain time period.

All changes to the business's assets, liabilities, equity, income, and expenses are recorded as journal entries in the general ledger.

Many bookkeepers and company owners employ software like, Wafeq - accounting system to keep track of debits and credits. That is because when manual ledgers are used to keep track of finances, mistakes are often made that lead to serious financial consequences.

FAQs About Debits & Credits

What is the difference between a creditor and a debtor?

A creditor is an individual or entity that extends a loan or provides goods or services on credit, expecting to receive payment in the future. A debtor is an individual or entity that receives a loan, goods, or services on credit and is obligated to make payments in the future.

How are debits and credits recorded in accounting?

Debits and credits are recorded using the double-entry bookkeeping system. Debits are always recorded on the left side of a general ledger sheet, while credits are recorded on the right side. The accounts are continually balanced to ensure that Assets always equal Liabilities plus Shareholders' Equity.

When is a person considered a creditor or a debtor?

A person or business becomes a creditor when they supply money, services, or products upfront without receiving immediate payment. They become debtors when they accept money, services, or products and commit to paying for them at a later date.

What is the importance of the double-entry system in accounting?

The double-entry system is crucial because it tracks every single business transaction in at least two separate accounts, providing an accurate, transparent view of a company's true financial health. Because total debits must always equal total credits, this system prevents balancing mathematical errors and forms the foundation of accurate financial reporting.

How do debit and credit accounts affect financial statements?

Debits and credits directly shape your Balance Sheet. An increase in debit entries typically boosts your Assets (like cash or accounts receivable) or expenses. An increase in credit entries boosts your Liabilities (like accounts payable), equity, or revenue.

What are common examples of debit and credit accounts?

- Debit Accounts (Assets/Expenses): Cash in bank, Accounts Receivable (invoices owed to you), inventory, and equipment.

- Credit Accounts (Liabilities/Revenue): Accounts Payable (bills you owe to suppliers), bank loans, and sales revenue.

How does using accounting software help manage debits and credits?

Accounting software automates the tracking of debits and credits with absolute precision. Instead of manually mapping double-entry journals, cloud platforms like Wafeq record transactions in the background the moment an invoice is raised or a bill is paid. This updates your financial statements in real time, eliminates human accounting errors, and gives you instant, audit-ready data.

Can an account have both debit and credit entries?

Yes. Most active accounts fluctuate constantly. For example, your Cash/Bank account is debited every time a customer pays you (cash increases) and is credited every time you pay rent or purchase inventory (cash decreases). The final net amount is what determines your account balance.

Wafeq Accounting- The best invoicing software keeps all accounts on track to run your business better.

Wafeq Accounting- The best invoicing software keeps all accounts on track to run your business better.

.png?alt=media)